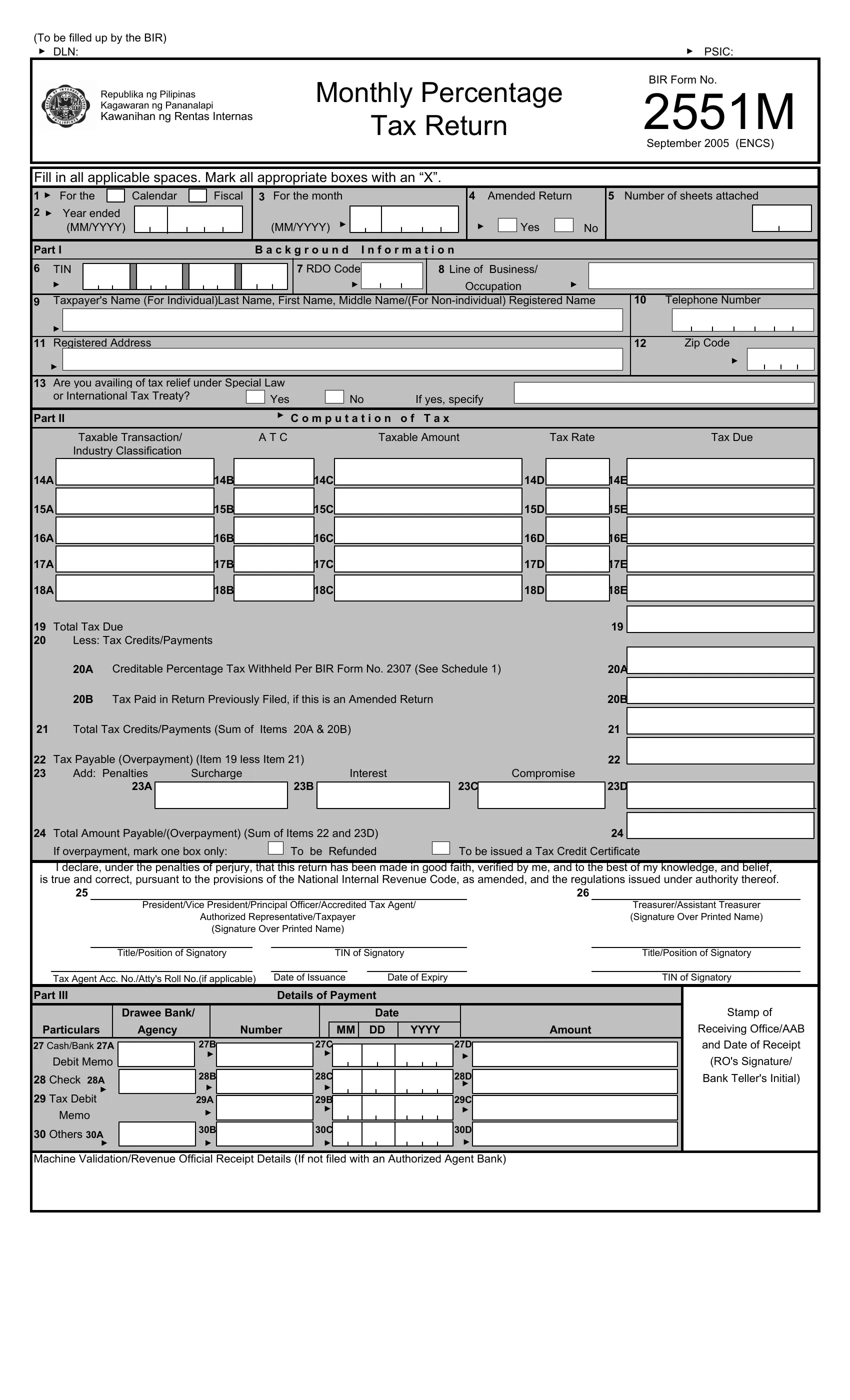

The Bureau of Internal Revenue (BIR) requires specific groups of taxpayers in the Philippines to file BIR Form 2551M each month. This form has been in use since September 2005 and covers the monthly percentage tax obligation for non-VAT registered individuals and entities.

Taxpayers whose annual gross sales or receipts do not exceed PHP 3,000,000 and who are not registered for VAT must file this form. The following groups are also required to submit BIR Form 2551M:

BIR Form 2551M must be filed and paid on or before the 20th day of the month following the taxable month. For example, the percentage tax for January is due by February 20. Taxpayers registered with the Electronic Filing and Payment System (eFPS) follow the same deadline. Late filing results in penalties, surcharges, and interest charges as specified in the National Internal Revenue Code.

Failure to file BIR Form 2551M on time triggers a 25% surcharge on the unpaid tax amount. If the BIR determines that the failure was willful, the surcharge increases to 50%. Interest of 12% per annum is also imposed on the unpaid tax from the due date until full payment. A compromise penalty may apply depending on the circumstances. Taxpayers who repeatedly fail to file risk additional enforcement actions from the BIR.

Taxpayers who file BIR Form 2551M often need to submit other BIR documents alongside their monthly percentage tax return. BIR Form 0605 is used for payment of annual registration fees. Those who employ workers must also file BIR Form 1601-C for monthly withholding tax remittance. At the end of the fiscal year, the BIR Form 1701 serves as the annual income tax return for self-employed individuals and professionals. Employers issue BIR Form 2316 as the certificate of compensation payment and tax withheld to their employees.

| Question | Answer |

|---|---|

| Form Name | BIR Form 2551M |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | 2551m deadline 2021, bir 2551m, bir 2551q form, 2551m |