Before starting Schedule R, gather information about your California sales (or gross receipts), California property values, and California payroll amounts. For corporations using the Water's-Edge election, also prepare your domestic (U.S.-based) income figures separately from worldwide totals. Our online PDF editor lets you complete California Schedule R quickly and easily.

Step 1: Hit the "Get Form" button above. It will open our editor so you can begin filling out the form.

Step 2: Once you open the editor, the document is ready to fill out. You can fill in blank fields, add custom text, insert images, sign the form, and more.

As for the blank fields of this specific PDF, here is what you should consider:

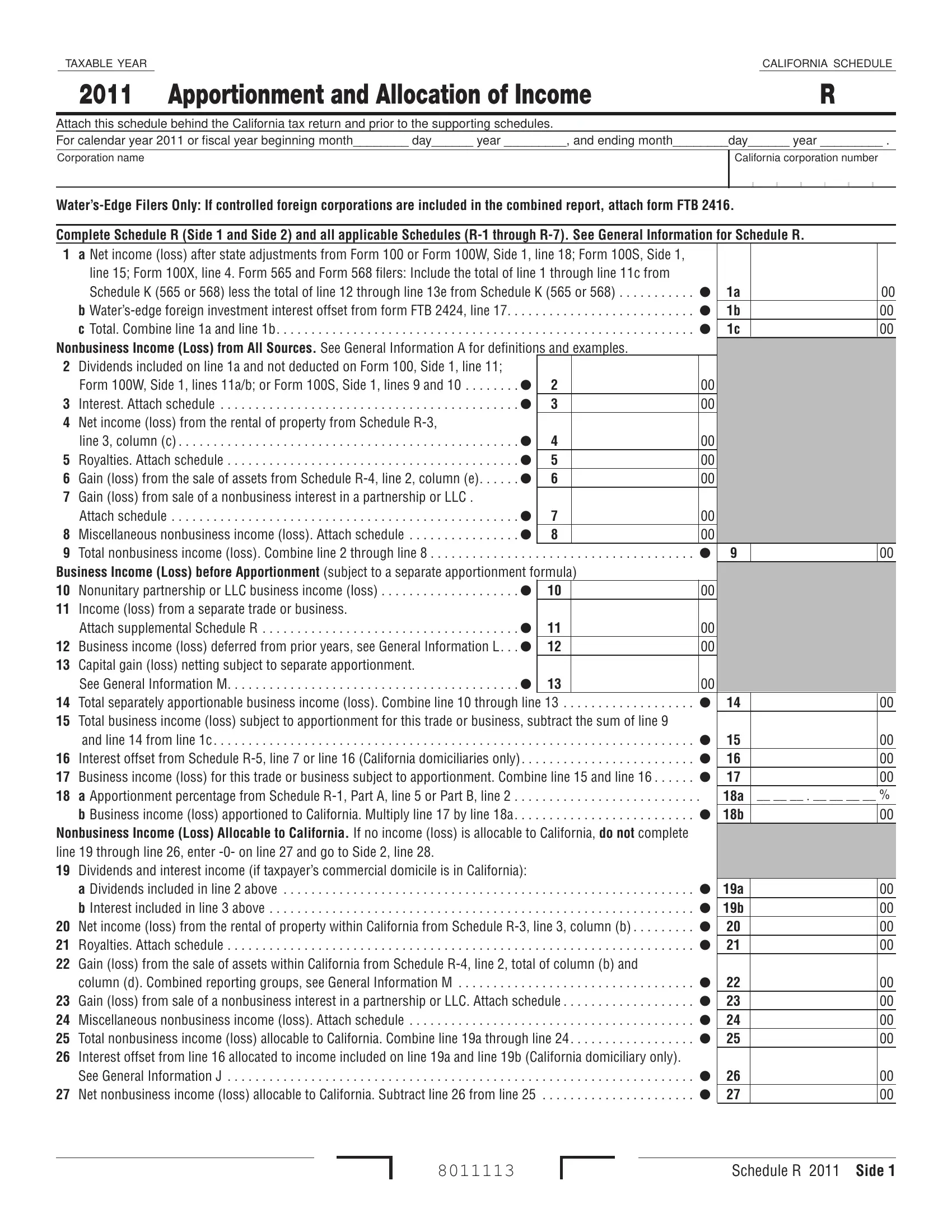

1. To start with, once filling in the california schedule r, start in the section that contains the next blank fields:

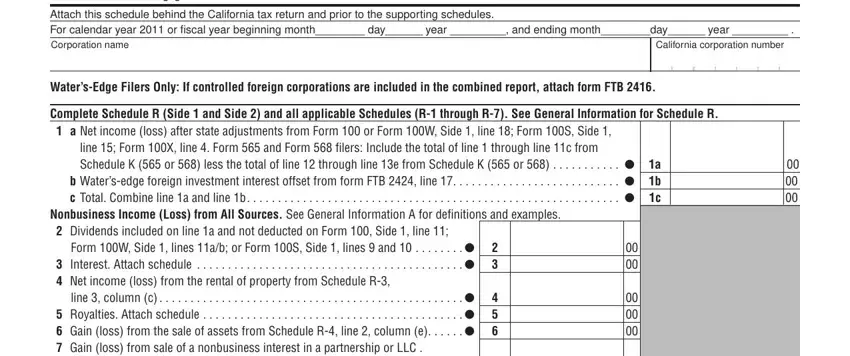

2. Given that the previous part is complete, you are ready to insert the needed particulars in Form W Side lines ab or Form S, Business Income Loss before, Capital gain loss netting subject, Income loss from a separate trade, Total business income loss, Total separately apportionable, a Dividends included in line, and Gain loss from the sale of assets so you can go further.

3. This next section is straightforward. a Dividends included in line, Interest offset from line, and Schedule R Side - every one of these empty fields is required to be filled out here.

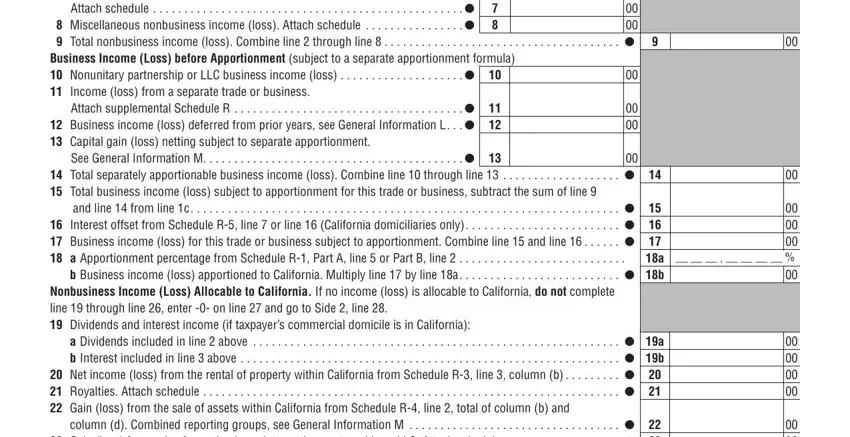

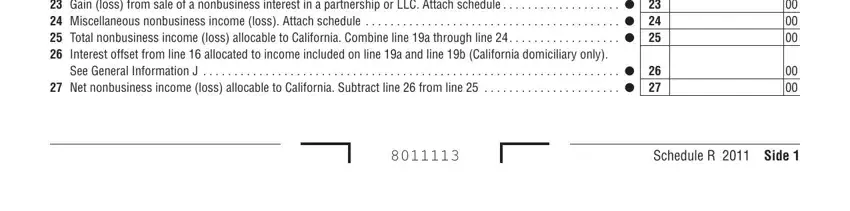

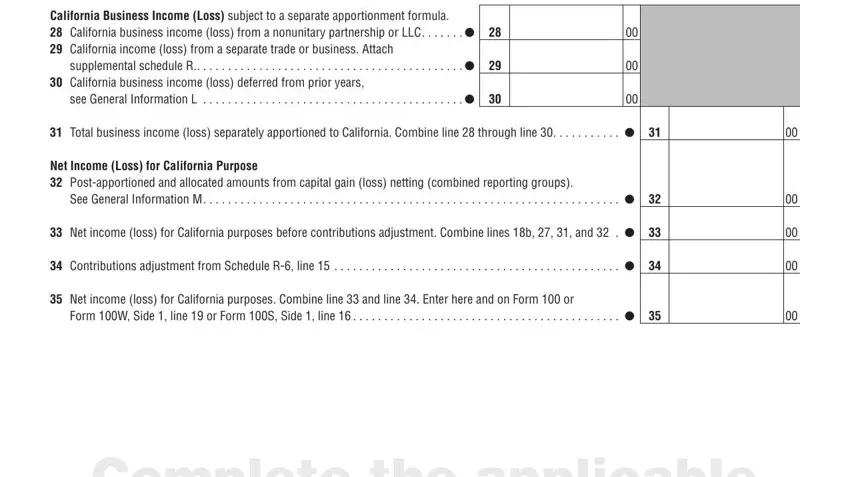

4. To go forward, this section requires filling in a few blank fields. Included in these are California Business Income Loss, California business income loss, California income loss from a, Total business income loss, Net Income Loss for California, See General Information M, Net income loss for California, Form W Side line or Form S Side, and Complete the applicable, which you will find fundamental to moving forward.

It is easy to make an error while filling out your Complete the applicable section, so review it carefully before you finalize the form.

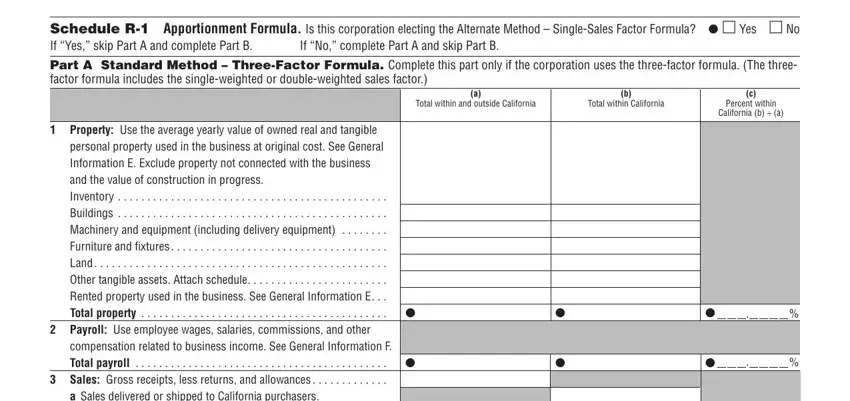

5. Lastly, this final subsection is what you will need to wrap up before submitting the document. The blanks include: Schedule R Apportionment Formula, If Yes skip Part A and complete, If No complete Part A and skip, Part A Standard Method, Total within and outside California, Total within California, Percent within, California b a, Total property, compensation related to business, Total payroll, Property Use the average yearly, and a Sales delivered or shipped to California.

Step 3: After reviewing all the information you entered, click "Done" to finalize your form. You can download, email, or save the completed California Schedule R directly from your FormsPal account.

Related California Tax Forms

California Schedule R is filed with or alongside these related tax documents:

- California Form 100-WE - Water's-Edge election form filed with Schedule R by corporations limiting apportionment to domestic income

- California Form 100S - S corporation franchise or income tax return, which may also require Schedule R for multi-state S corporations

- California Schedule P - Alternative Minimum Tax schedule for California residents and certain corporations

- California 540 Schedule CA - Individual income adjustment schedule for California residents

Frequently Asked Questions About California Schedule R

What is California Schedule R used for?

California Schedule R is used by corporations to apportion and allocate income between California and other states. It determines what percentage of a corporation's total business income is subject to California franchise or income tax, based on the corporation's California sales, property, and payroll relative to its totals from all states.

Who is required to file Schedule R?

Any corporation that has income from California sources and income from outside California must file Schedule R with their Form 100 tax return. This includes C corporations, corporations making a Water's-Edge election, and limited liability companies taxed as corporations with multi-state operations.

What is the single-sales factor apportionment formula?

The single-sales factor formula calculates California's share of a corporation's income based on the percentage of total sales attributed to California customers. If a corporation has total sales of $1 million and $300,000 in California sales, California would tax 30% of its business income. This is the standard apportionment method for most California corporations.

What are Schedule R supplemental schedules R-1 through R-7?

The supplemental schedules handle specific income situations. R-1 covers apportionment for banks and financial institutions. R-2 addresses income from installment sales. Other schedules cover interest offsets, nonbusiness income allocation, dividends, and deductions related to sales of assets across multiple tax periods.