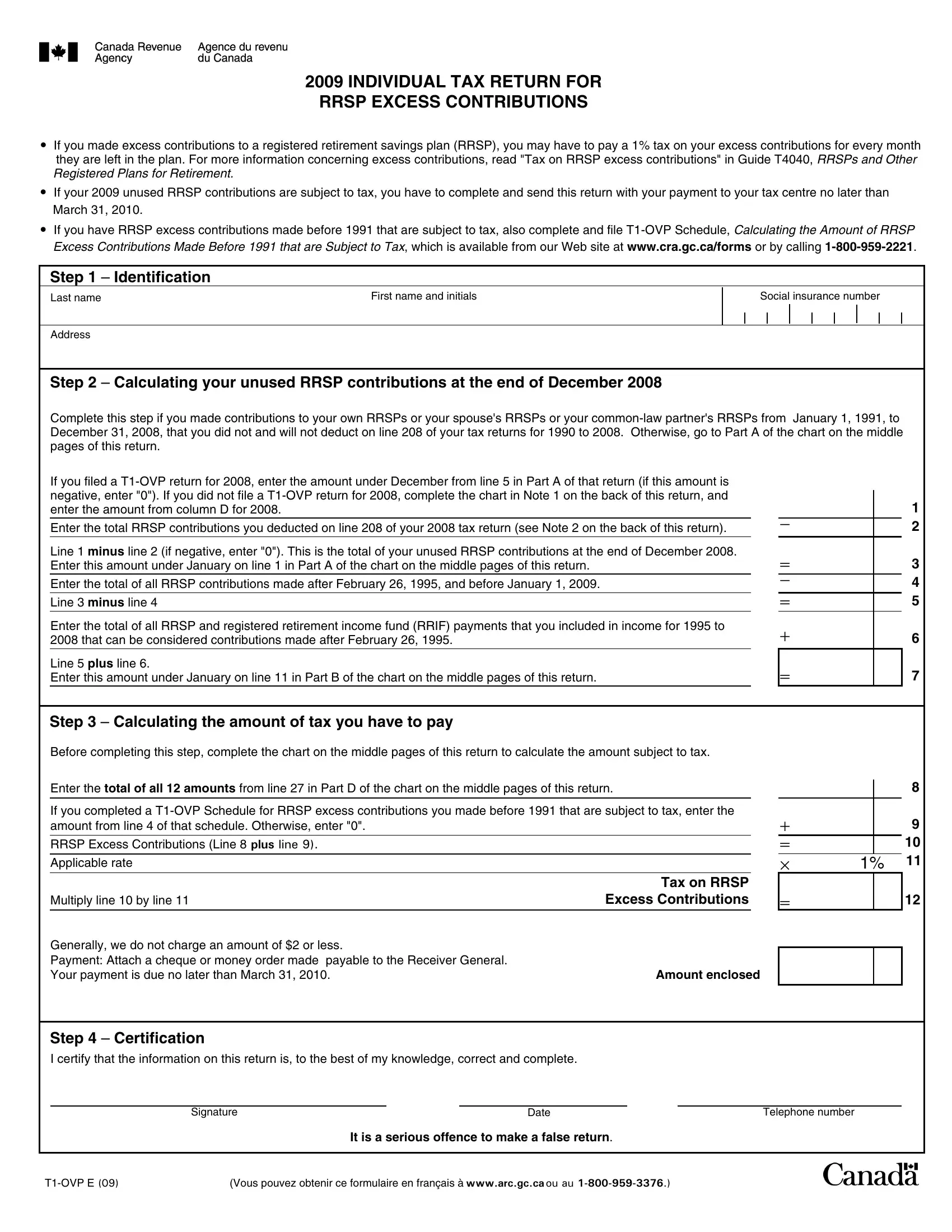

The T1 OVP E form has four sections covering identification, excess contribution calculations, monthly tax computation, and certification. Follow the steps below to complete each part correctly.

Steps to Complete the T1 OVP E Form

- Section 1 - Identification: Enter your full legal name, social insurance number (SIN), and current mailing address.

- Section 2 - Excess contributions: Record your total RRSP contributions for the year and subtract your available deduction room. The difference is the excess amount subject to the 1% monthly tax.

- Section 3 - Monthly tax computation: For each month the excess remained in your RRSP, calculate 1% of the highest excess balance during that month. Add all monthly figures to find the total tax owed for the year.

- Section 4 - Certification and payment: Review the completed form, sign the certification, and attach any payment owed. Mail the form and payment to your CRA tax centre by March 31.

Frequently Asked Questions

What is the penalty for missing the T1 OVP E deadline?

The CRA charges a 5% late-filing penalty on the outstanding balance plus 1% of that balance for each complete month the return is overdue, up to 12 months. Daily compound interest also applies to any unpaid tax amount.

Can I withdraw the excess RRSP amount to stop the penalty?

Yes. Withdrawing the excess contribution stops the 1% monthly tax from accumulating going forward. The withdrawn amount is added to your taxable income for that year, so consider speaking with a tax professional before taking this step.

Where can I find other related Canada tax forms?

If you are transferring funds between registered plans, the Canada Form T2220 E handles RRSP-to-RRSP transfers. For corporate income tax, visit the Canada T2 Tax Form page. You can also explore Canada Form T2062 for other CRA filings.