FormsPal's online editor lets you open, fill in, and download Canada Form T2220 E without printing or mailing anything. Follow the steps below to complete this two-page CRA document correctly.

Steps to Complete Form T2220 E

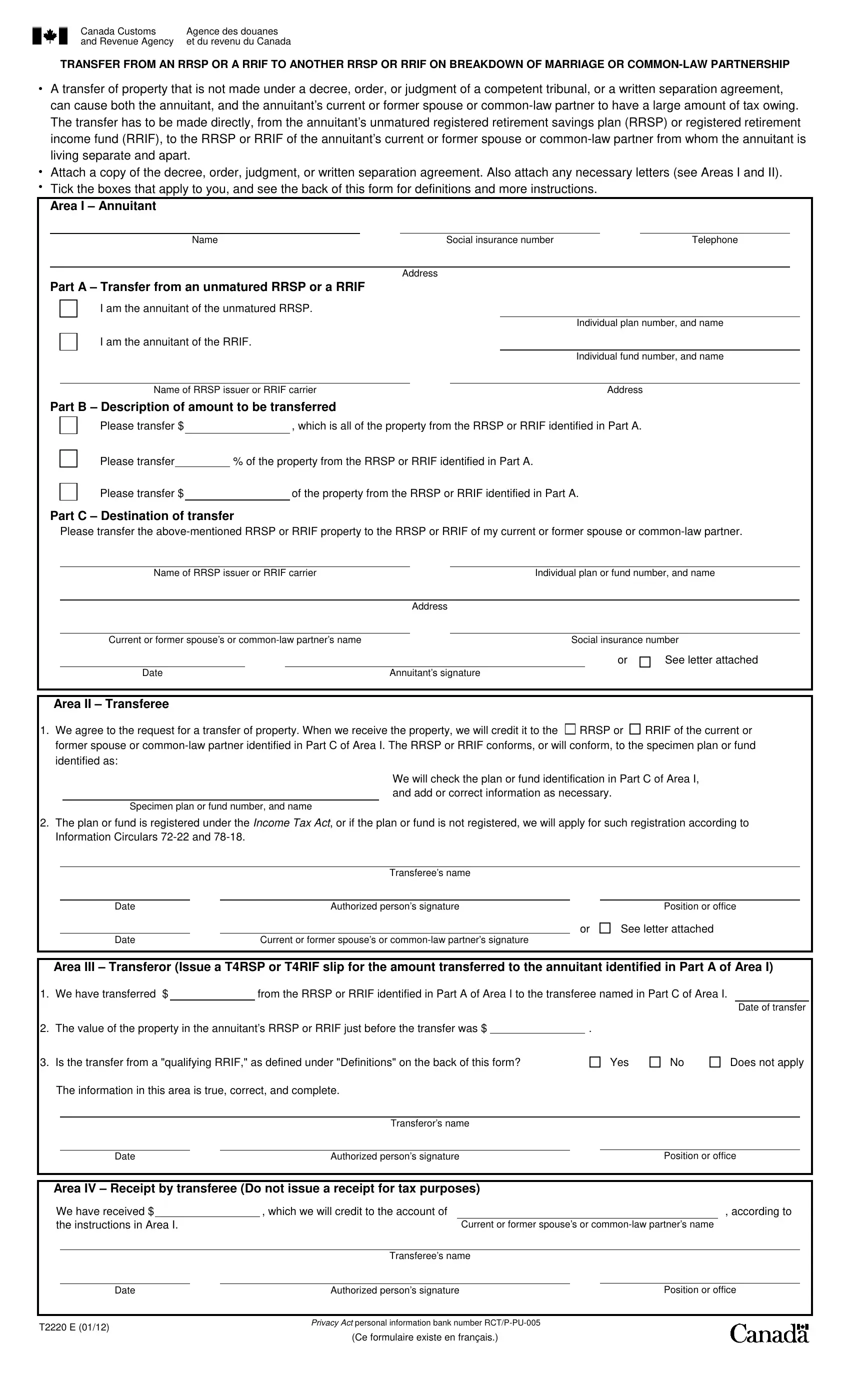

Step 1: Gather your supporting documents. Before starting, locate your legal separation agreement, divorce decree, or court order. The CRA requires this document to be attached to the completed T2220 E form.

Step 2: Fill in the annuitant's details. Enter the full legal name, social insurance number (SIN), and address of the person whose RRSP or RRIF is being transferred. Include the plan number and the name of the financial institution or plan issuer.

Step 3: Enter the recipient's plan information. Provide the spouse or common-law partner's full name, SIN, and the receiving plan number with the issuer's name. The recipient's financial institution will need these details to accept the incoming transfer.

Step 4: Specify the transfer amount. Indicate whether you are transferring the entire plan balance or a specific dollar amount. Both parties must sign the form in the spaces provided before submission.

Step 5: Submit to the plan issuer. Do not send Form T2220 E to the CRA. Submit the signed form and your supporting legal document to the RRSP or RRIF issuer. The issuer processes the transfer and files a T4RSP or T4RIF slip with the CRA.

Frequently Asked Questions About Form T2220 E

What does Form T2220 E authorize? It authorizes a direct, tax-deferred transfer of RRSP or RRIF property from one spouse to another after a marriage or common-law partnership breakdown. Without this form, the transfer would be treated as a withdrawal and taxed in the year it occurs.

Who must sign Form T2220 E? Both the annuitant (the transferring spouse) and the recipient (the receiving spouse) must sign the form. The plan issuer also completes a section confirming the transfer details.

Do I send the form to the CRA? No. Submit the completed Form T2220 E directly to your RRSP or RRIF financial institution. The issuer reports the transfer to the CRA using a T4RSP or T4RIF information slip.

What supporting documents are required? You must attach a copy of the legal agreement authorizing the transfer, such as a signed separation agreement, court order, or divorce judgment. Transfers without this documentation will not be processed.

You may also need to complete other Canadian financial and tax forms during a relationship breakdown. See our guides for the Canada T1 OVP E form, the Canada T2 tax form, and the Canada TD1 form.