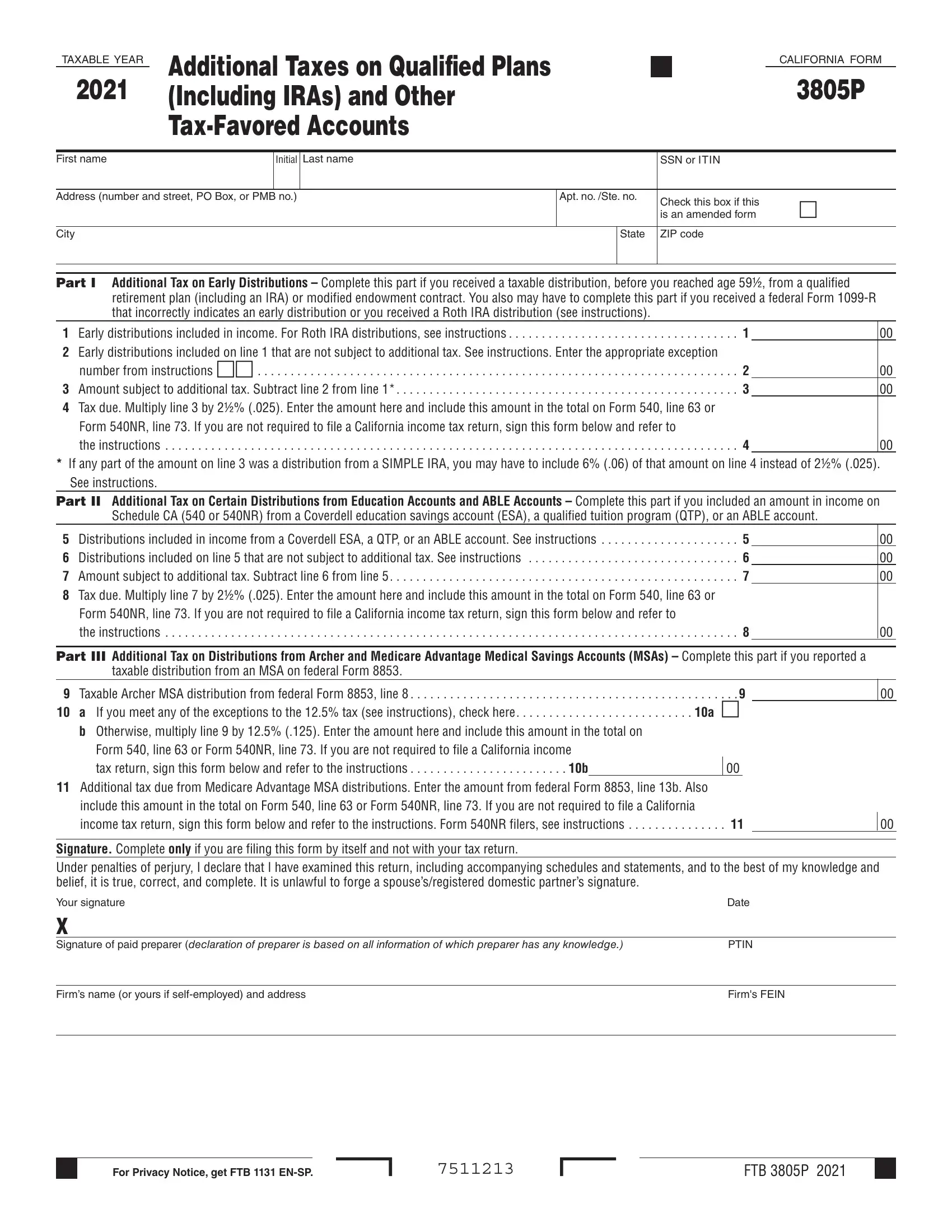

The 3805P form, an essential document for individuals in California dealing with additional taxes attributable to IRAs, other qualified retirement plans, annuities, modified endowment contracts, and MSAs for the year 2000, serves a crucial role in tax reporting and compliance. Its primary purpose is to detail any taxes owed due to early distributions taken from these financial instruments before reaching the age of 59½, alongside distributions from Ed IRAs not utilized for educational expenses and taxable distributions from Medical Savings Accounts (MSAs). It's vital for individuals who received taxable distributions from any of these accounts or who need to rectify incorrect exception codes on their Form 1099-R. This form’s distinct sections allow taxpayers to calculate additional taxes due, conforming predominantly with federal tax laws but with notable exceptions specifically tailored to California’s tax regulations. Not only does the form accommodate for jointly filed returns by requiring separate forms for each spouse, but it also delineates specific filing instructions for individuals who may not need to file a California income tax return but still owe taxes according to the form’s guidelines. Furthermore, the 3805P form addresses contributions and distributions nuances, like rollovers, that are tax-exempt under specific conditions. Understanding the intent and the detailed instructions of the 3805P form is indispensable for residents to navigate their tax obligations effectively concerning retirement plans and accounts in California.

| Question | Answer |

|---|---|

| Form Name | Form 3805P |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | 2000, FTB, 540NR, MSA |