|

explanation of gain/loss items, but do not submit the federal |

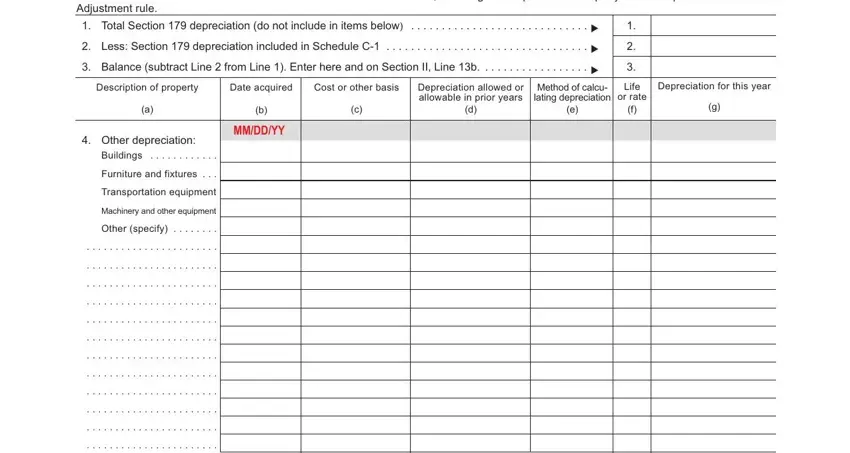

any differences in depreciation related to differences in basis |

|

schedule. |

of assets, amount of allowable Section 179 expense, or |

|

FORM 8271 |

method of depreciation for federal or PA purposes; and any |

|

other reductions in federal expenses allowed at 100 percent |

|

Do not report or deduct any transactions related to tax |

|

for PA personal income tax purposes. |

|

shelters. |

|

|

|

|

FORM 8594 |

Examples of items that Pennsylvania requires as reductions |

|

in federal income or expenses include: income taxes based |

|

Report the acquisition or disposition of business assets on |

|

upon gross or net income; any differences in depreciation |

|

Line 4 of PA Schedule C. Refer to the federal schedule for |

|

related to differences in basis of assets, amount of allowable |

|

an explanation for gain/loss items, but do not submit the |

|

Section 179 expense, or method of depreciation for federal |

|

federal schedule. |

|

or PA purposes; recognition of cancellation of debt income; |

|

|

|

|

|

FORM 8824 |

recognition of income from IRC Section 481(a) spread |

|

Do not report a like-kind exchange on PA Schedule C. PA |

adjustments; payments for owner pension, profit-sharing |

|

law does not have like-kind exchange provisions. You must |

plans, deferred, or welfare benefit plans; percentage deple- |

|

include the gain or loss from a sale, exchange or disposition |

tion; direct expensing of organizational expenses or syndi- |

|

of a business asset on Line 4 of PA Schedule C if the trans- |

cation fees; losses from the sale of property where PA basis |

|

action was a normal business transaction. You must report |

is different than federal basis; and any other income or |

|

any gain or loss from the sale of a nonbusiness asset or |

expenses where there is a specialized federal treatment that |

|

property or the sale of a business or segment thereof on PA |

is not specifically addressed or allowed by PA personal |

|

Schedule D if the property sold was not replaced. |

income tax law that might involve additional expensing, |

|

FORM 8829 |

expensing verses capitalization, carry back or carry forward |

|

of losses, income recognition, or other special treatments. |

|

Include your allowable expenses for the business use of |

|

Other differences between Pennsylvania and federal income |

|

your home on Line 37 of PA Schedule C. Refer to the federal |

|

schedule for an explanation of this expense, but do not sub- |

tax include the following: |

|

mit the federal schedule. Pennsylvania does not recognize |

IDCs. Special rules apply for the direct expensing of intan- |

|

the federal safe harbor method for determining the allowable |

gible drilling & development costs (IDCs). Up to one-third of |

|

deduction for business use of a residence for Pennsylvania |

the amount of IDCs incurred in tax years beginning after |

|

Personal Income Tax purposes. All home office expenses |

Dec. 31, 2013 may be directly expensed, with the remaining |

|

must be determined by using actual costs incurred. |

amount amortized over 10 years. Taxpayers may also elect |

|

|

|

|

to amortize the full amount of the IDCs over 10 years. The |

|

|

OTHER PENNSYLVANIA AND FEDERAL |

|

election to expense any IDCs is made by including an |

|

|

|

amount on Line 34 of PA Schedule C. Amortization of the |

|

|

INCOME TAX DIFFERENCES |

|

|

|

|

IDCs must be reported separately on Line 35 of PA Schedule |

|

|

|

|

|

PA income from the operation of business generally differs |

C. IDCs incurred prior to Jan. 1, 2014 must be amortized |

|

over the life of the well. |

|

from the income determined for federal income tax purposes. |

|

|

|

|

Further, Pennsylvania will no longer accept a PA Schedule |

Qualified Joint Ventures. Pennsylvania is not a community |

|

C-F Reconciliation for the purpose of adjusting the federal |

property state. Therefore, for PA personal income tax |

|

business income to PA business income. Therefore, the |

purposes, a taxpayer and the taxpayer’s spouse must each |

|

items which were previously included as additions to PA |

report on a separate PA Schedule C their share of income |

|

income or expense on the PA Schedule C-F Reconciliation |

from a business entity they own that is considered a qualified |

|

should be included with the specific line of income or |

joint venture for federal income tax purposes. |

|

expense on the PA Schedule C. In addition, those items |

|

|

|

which Pennsylvania does not require be reported as income |

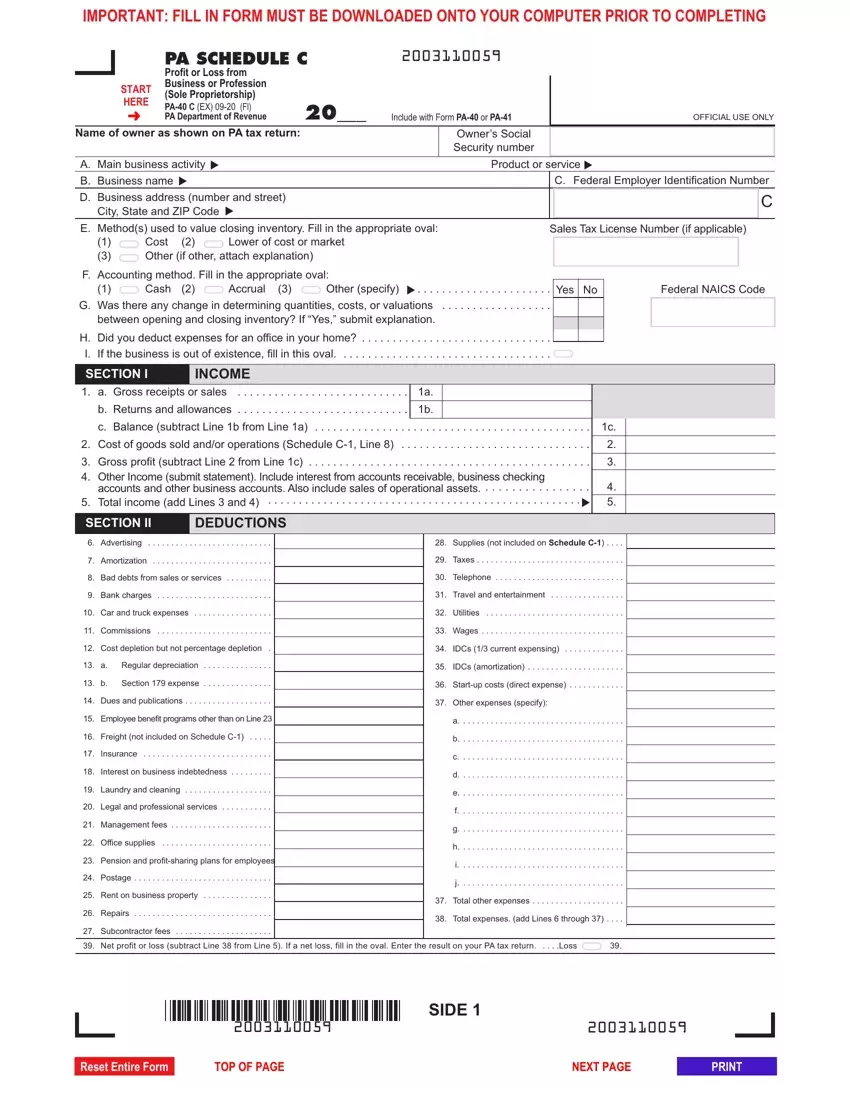

LINE INSTRUCTIONS |

|

|

or does not allow as expense in determining net business |

|

|

|

|

|

|

income, which are allowed in the determination of net federal |

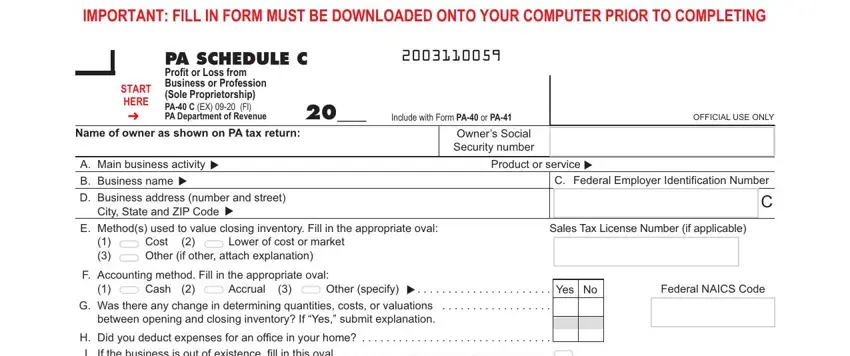

IDENTIFICATION INFORMATION |

|

business income, should not be included in the specific |

Complete each line. |

|

business income or expenses on PA Schedule C. |

OWNER'S NAME |

|

|

|

|

|

Examples of items that Pennsylvania requires as additions |

Enter the name of the business owner. If you are married |

|

to income include: any advance receipts for goods or serv- |

and you jointly owned the business with your spouse, you |

|

ices; working capital interest or dividend income including |

must complete separate PA Schedule C’s. If you and your |

|

federal-exempt interest and dividend income from obliga- |

spouse have separate business activities, complete separate |

|

tions of other states; gains from the sale of business assets |

PA Schedule(s) C. |

|

where the property is replaced by similar property; gains |

SALES TAX LICENSE NUMBER |

|

from like-kind exchanges; gains from involuntary conver- |

|

Enter your Pennsylvania Sales Tax License Number if you |

|

sions (such as those from IRC Section 1033); and gains |

|

have one. Otherwise, leave this space blank. |

|

from the sale of property where PA basis is different than |

|

|

|

|

federal basis. |

FEDERAL NAICS CODE |

|

Examples of items that Pennsylvania allows as additions to |

Provide your Federal NAICS Code as identified on your |

|

Federal Schedule C. |

|

expenses that require a reduction for federal tax purposes |

|

|

|

|

include: meals, travel and entertainment expense deduction |

SOCIAL SECURITY NUMBER (SSN) |

|

of 100 percent by Pennsylvania for the expenses incurred; |

Enter the SSN of the business owner. |

|

|

|

|

|

|

|

2 |

PA-40 C |

www.revenue.pa.gov |

Other (if other, attach explanation)

Other (if other, attach explanation)