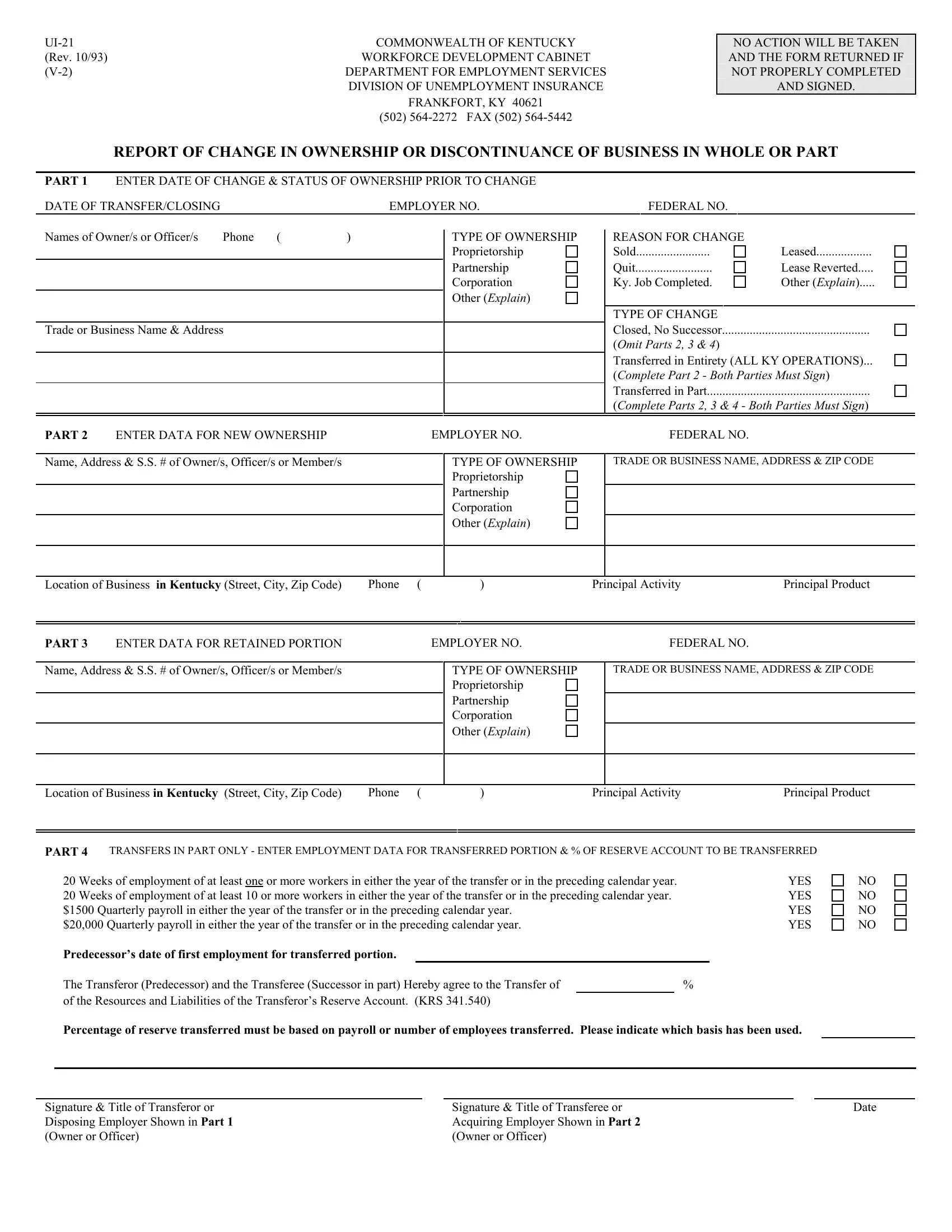

At the heart of navigating the evolution or cessation of a business in Kentucky lies the comprehensive UI-21 form, a critical document forged by the Commonwealth of Kentucky's Workforce Development Cabinet, Department of Employment Services. This form serves as a pivotal tool for reporting any changes in ownership or the discontinuation of a business, either in part or in its entirety. It meticulously gathers details from the date and nature of the ownership change to the specifics surrounding the type of ownership and the reasons prompting these shifts. By dissecting the varied components—ranging from the entirety transfer to the nuanced division of business assets and liabilities—it lays a structured pathway for ensuring that the transfer or cessation process adheres to the state’s legislative framework. Beyond the operational changes, the UI-21 form delves into the allocation of resources and liabilities of the predecessor's reserve account to the successor, underpinned by Kentucky Revised Statute 341.540, illustrating a balance of continuity and financial responsibility amidst transitions. The rigorous requirement for comprehensive completion and signing off by involved parties highlights the form’s critical role in not just reporting but effectively managing the implications of business ownership changes on employment and contribution obligations within Kentucky. As a linchpin in the administrative process, the UI-21 form embodies an essential procedure for businesses navigating the complex landscape of ownership transition or cessation, ensuring legal compliance and the smooth transition of obligations in the ever-evolving business environment.

| Question | Answer |

|---|---|

| Form Name | Form Ui 21 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | Transferor, acquirers, Transferee, UI-21 |