The PDF editor helps make filling out forms simple and easy. It is very effortless to enhance the [FORMNAME] document. Use these particular steps if you would like do it:

Step 1: Choose the orange "Get Form Now" button on the following page.

Step 2: The document editing page is now available. You can include information or modify current content.

Fill in the wv tax form cd 3 PDF by entering the information necessary for every section.

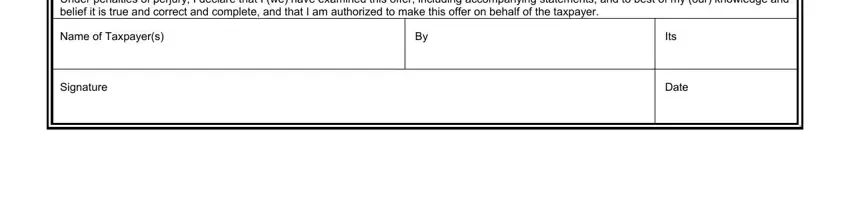

Type in the demanded data in the field Under penalties of perjury I, Date, and Its.

Step 3: Click "Done". Now you may export the PDF form.

Step 4: You will need to generate as many copies of the document as possible to avoid potential complications.