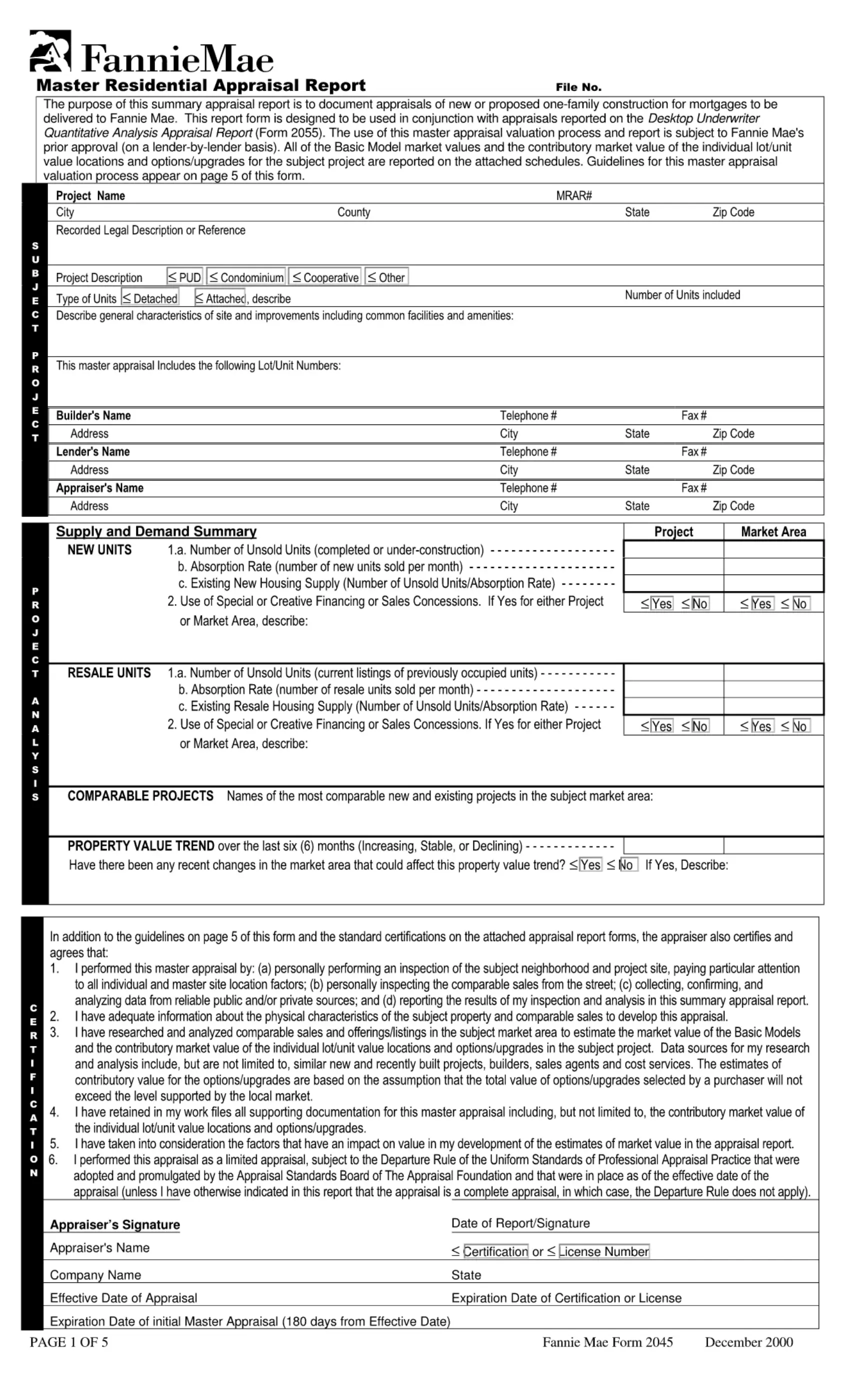

Follow the steps below to complete the 2045 Appraisal Form correctly and submit it to your lender.

Step 1: Enter Subject Property Data

Record the full property address, legal description, and current owner name. Indicate whether the property is a single-unit residence or a single-unit PUD. Note the loan type: purchase money mortgage or non-owner occupied refinance.

Step 2: Describe Property Characteristics

Enter the year built, lot size, total gross living area, and room count. Include the number of bedrooms and bathrooms. Record the property's overall condition using the standard rating scale.

Step 3: Document Market Conditions

Summarize local supply and demand trends for the subject's neighborhood. Note whether the market is expanding, stable, or declining. Include the typical marketing time for similar properties in the area.

Step 4: Select and Analyze Comparable Sales

Choose three to five recent sales of similar properties. Comparables should be from the same neighborhood or a competing area and sold within the past 12 months when possible. Adjust each comparable for differences from the subject property, including location, gross living area, condition, and features such as a garage or pool.

Step 5: Reach a Value Conclusion

After analyzing the comparables and making adjustments, enter your final market value estimate. Sign and date the certification section. Submit the completed form to the requesting lender.

For related mortgage documents, see the 71B Rev Appraisal Form and the FHA Refinance Authorization Form.