The Substitute Form 1099-S is a tax document in the United States that provides details on the proceeds from real estate transactions. The form is issued by the person responsible for closing a real estate transaction, which could be a title company, a real estate agent, or an attorney.

The form includes information such as the gross proceeds from the sale (generally the selling price), the date of closing, a description or address of the property, and whether the seller received property or services as part of the transaction, among other details. The person responsible for the closing of the transaction must furnish this statement to the seller, or “transferor”.

The form is used to report the transaction to the Internal Revenue Service (IRS), and the person who sold the property (the transferor) may need to report the transaction on their income tax return. The specifics of whether the transaction needs to be reported, and how, depend on various factors such as whether the property was the seller’s main home and whether they had a gain or loss from the sale.

The filer shall refer to the US Internal Revenue Code (IRC) regulations in reporting their current real estate proceeds. The IRS tends to amend its legal regulations quite frequently. Therefore we strongly advise you to check for updates (as well as the specific state’s amendments) from time to time.

The IRS has worked out General Instructions for Certain Information Returns. They have sections containing detailed information on each IRS form. You can always refer to these rules for help if you happen to have doubts in a particular situation. However, there are some basic guidelines and principles that one has to keep in mind.

First up, you must always require the trader’s Taxpayer Identification Number (TIN) before or upon the deal’s closing date. Once you complete the transaction, you will have to insert this information in the form.

The second important thing to keep in mind is that the filer needs to compile a transferring statement and deliver it to the seller or the transferor. If there are several sellers, you should pick up a relevant copy of the 1099-S Form and send one to each of them.

You can never charge your customers extra for complying with the IRS 1099-S Form proceedings. The law only allows you to take the costs of filing into account. You can then include those fees as customer service into the whole real estate transaction’s gross total cost.

When making any corrections to your Proceeds from Real Estate transactions IRS reports, please make sure that you are amending the corresponding year form. Corrections for the previous financial periods must be made on the previous year’s IRS 1099-S Forms. You can refer to the 2021 General Instructions for Certain Information Returns for details.

Normally, the person closing the deal is responsible for filling out and filing the 1099-S Form to the relevant IRS office. If the responsible person is absent for some reason, this person’s trustee can handle all the paperwork. It may be (specifically in that order):

Neither an employee nor an agent can participate in a real estate deal on their own. Only the employer or the principal can be qualified as the reporting person.

As we have established above, foreigners making real estate transfers in the United States territory shall also report their transaction income to the IRS with the 1099-S Form. For more details on withholding taxes from foreign residents and their liability, refer to Publication 515 of the IRC.

You may participate in a real estate deal involving multiple transferors. In this case, just fill out and file separate 1099-S Form copies for each seller. You must also ask the transferors (orally or in writing) for the allocation agreement of the estate’s gross profits.

As to partnership-owned property, you only need to fill out and file one 1099-S form for one partnership-owned piece of property that you are acquiring.

If you decide to purchase a piece of residential property from spouses, you should view them as a single-tenant, regardless of whether they stay together at the transaction closing or divorced. Therefore, you only require one 1099-S form to provide for them. You also do not need a proceeds allocation from them.

Anyone putting a signature on the form must keep the copy for at least four years. The reporting person must attach a Closing Disclosure to the form prescribed under the Wall Street Reform and Consumer Protection Act. Make sure to double-check if the disclosure is present.

Using the 1099-S Form, you can report the full or partial sale of your residential property, exchange of the property for a certain money equivalent, indebtedness, or other services that can be defined as a transaction. You may use the form to report the income from the following kinds of residential property:

Further, we are going to consider the ownership change circumstances under which you do need to file the 1099-S Form.

Once you have traded your real estate for money, part of it automatically belongs to the federal income through taxes. Residential property transfer to a corporation also qualifies as a nonrecognition of gain under section 351 of the state Internal Revenue Code. Therefore, all the above cases are matters of reportable real estate exchange.

Those who obtain any kind of real estate ownership interest shall also report the income in the current financial period to the Revenue Service office. The rule applies to the previously acquired ownership rights to possess or use the residential property for the term of at least 30 years in a row.

According to section 6050-N of the Internal Revenue Code, anyone who is receiving payments for timber royalties via a pay-as-cut contract shall report them using the 1099-S Form in the current financial period.

It sometimes happens that an owner is forced to exchange or trade his or her personal residential property under pressure, such as condemnation, a threat of imminence, seizure, or requisition. However, even if the transaction took place under such circumstances, it still is subject to a tax report.

There are several exceptions to the general estate proceeds reporting rule. There are the following ones:

You can always use legal help to fill out the 1099-S paperwork, or you can use our latest software developments to tailor a corresponding form.

Follow our guidelines:

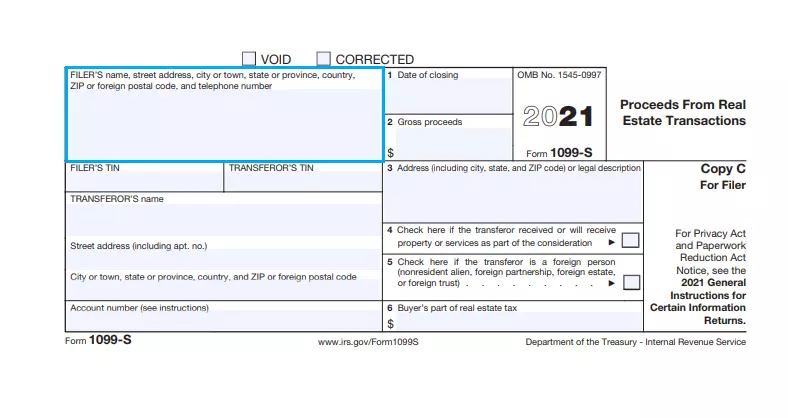

In this section, insert the filer’s full name, physical address, contact cell-phone number of the reporting person.

Insert the Taxpayer ID Number of both the filer and the transferor in the corresponding sections (as shown below).

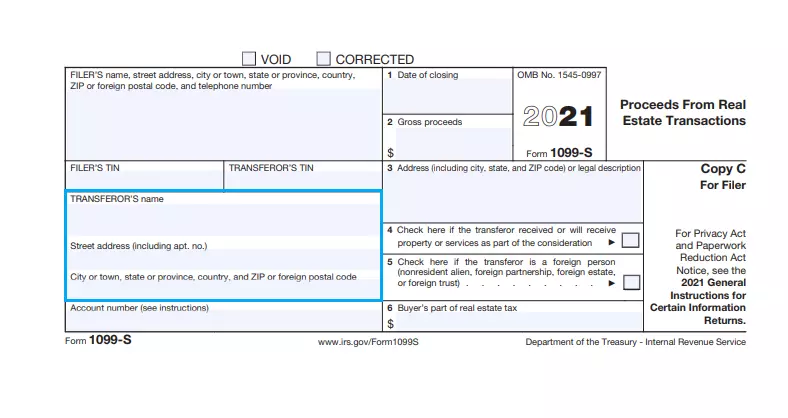

Fill in the seller’s full legal name and physical address. Remember that if you are acquiring the property from spouses, only one of them has to provide information.

The IRS encourages the filers to provide their account numbers. Enter one account number per document if you happen to have several of them.

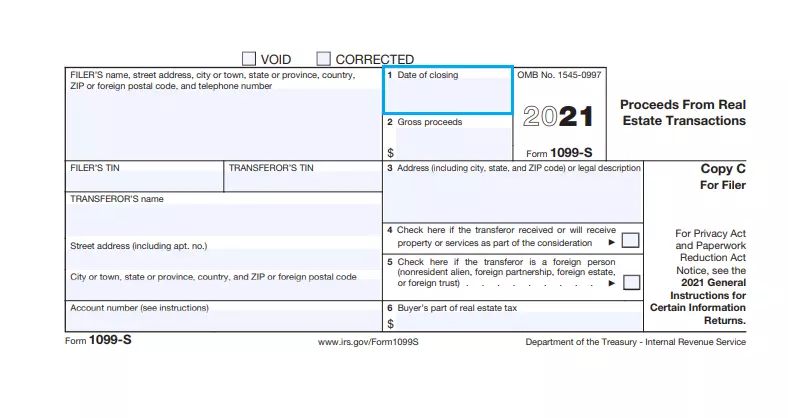

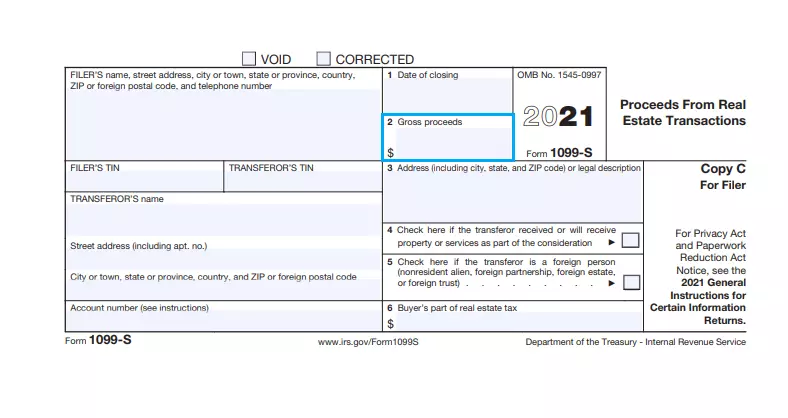

In this section, enter the deal’s closing date. It may differ from the closing date on the Closing Disclosure.

You should be very accurate in filling out this section. Enter the amount of gross profit that you have received from real estate. If you are reporting an equal property exchange, insert a “0” in this section and an “X” in Box number 4.

Please note that the gross real estate benefits amount does not include the costs of property-related services provided by the seller to the buyer (or the receiver). You may check with the instruction for filling out the details of a contingent payment deal.

Enter the physical address or any other relevant legal description of the subject property. For referring to timber royalties, use the title “Timber Royalties” before the address.

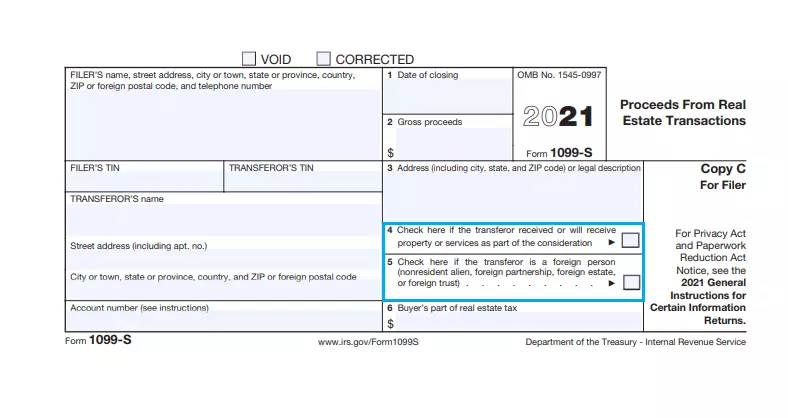

Check Box 4 if the seller already has received or is about to receive real estate or property-related services as part of the deal (equal value exchange). Check Box 5 if the seller is a foreign citizen.

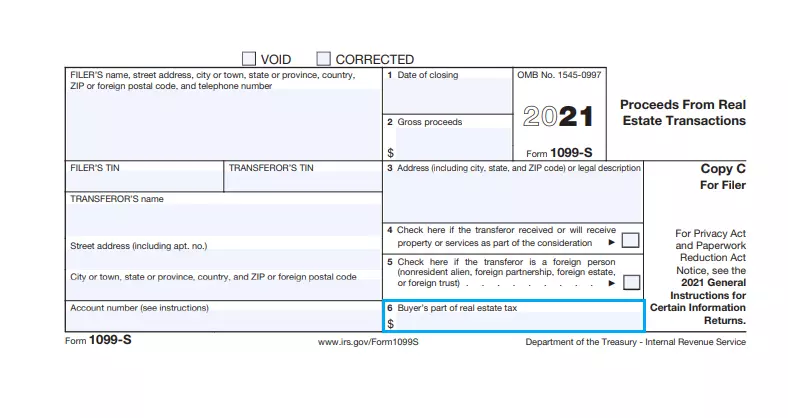

If the subject property is residential, the buyer must insert their share of the property tax in Box 6. It applies to cases when the real estate is paid in advance in the previous financial period. For example, sometimes people sell their residential property in a state or a county where the law requires them to pay the estate tax in advance annually.

You may also use the tax information indicated on the Closing Disclosure.